Launch of PFM Reporting Framework version 2.0

Background

At the 2016 INCOSAI, members committed to make a meaningful contribution to the Sustainable Development Goals (SDGs). One such contribution, is to rethink the way in which supreme audit institutions (SAIs) audits and reports on public financial management (PFM).

Sound public financial management, as a catalyst for government performance, is crucial to achieve the SDGs. Functioning PFM systems:

- ensure government finances are sustainable,

- allow for budgets to reflect political priorities and

- ensure efficient service delivery.

Against this backdrop, AFROSAI-E and GIZ jointly developed the PFM Reporting Framework. This tool allows SAIs to report holistically on country public financial management risks. At the May 2018 Governing Board meeting, members resolved to issue the PFM Reporting Framework as an official working tool which all member-SAIs may choose to use. Through the 15 SAI-led pilots of the tool, it was concluded that it is user-friendly, a good way to increase innovation of SAI audits, and primarily designed with the aim of increasing the value addition of the SAI audit process.

Using the feedback from these 15 SAIs, the AFROSAI-E / GIZ team have been working together with subject matter experts from various SAIs, to improve the tool. Three main areas where successfully addressed:

(a) Technical issues with the excel formulae in data capturing.

(b) Improved ability and agility of the tool to audit SDG implementation.

(c) Improved consistency and robustness in the audit of disaster preparedness of government institutions.

We are pleased to now announce the launch of: The PFM Reporting Framework version 2.0.

What is the PFM Reporting Framework version 2.0?

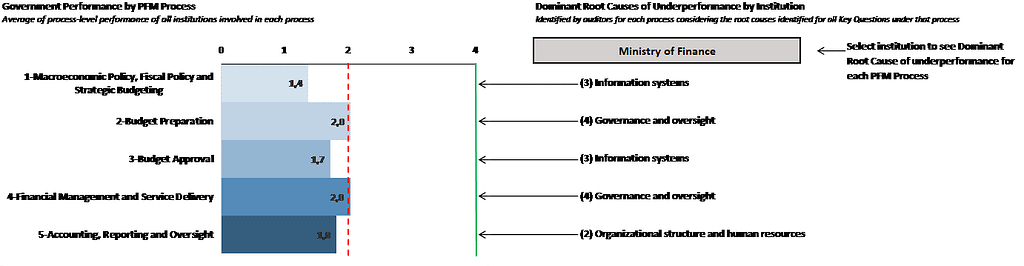

Version 2.0 is an improved version of the original tool. It is still excel-based, which allows auditors to assess the performance of PFM processes along the whole budget cycle. It is inspired by existing assessment frameworks like Public Expenditure and Financial Accountability, while catering for the specificities of the work of SAIs. The assessment covers core PFM policy making institutions such as the Ministry of Finance, Parliament and Revenue Authority, as well as important sector ministries and departments. These spending ministries are selected based on their potential contribution to the achievement of the SDGs and typically, includes the Ministries of Health and Education.

The Framework considers the different roles of the entities involved in PFM and allows auditors to assess the PFM performance of each of them. For each assessment question the auditor selects a level of performance which is then graded and automatically converted into a graphic dashboard presenting the results e.g.:

Key changes: SDG implementation and disaster preparedness audits

From a thematic perspective, the key focus of the tool is to engage SAIs to deliberately perform audits on the attainment of SDG targets at both ministerial and national levels. This focus is achieved in two ways.

- Firstly, within context. The tool has specific questions that provoke audit procedures from the auditors, which address the attainment of SDGs. In total the tool has 22 questions on SDG implementation, allocated between core and non-core ministries as follows:

- 8 Questions for the Ministry of Finance

- 5 Questions for the Revenue Authority

- 3 Questions for Parliament

- 6 Questions for all non-core ministries, departments and government agencies

- Secondly, within subtext, knowing fully well that prioritisation lies at the bedrock of the attainment of SDGs. The tool systematically allows a SAI to choose which SDG key ministries to audit annually, in line with country plans and expectations.

In the wake of the COVID19 pandemic, AFROSAI-E commenced with a research project on: SAI Resilience in addressing the auditor expectation gap during disaster periods: The case of sub-Sahara African SAIs during the COVID19 pandemic. While the research is still being finalised, initial indications show that in the past seven years, few SAIs had performed audits on disaster preparedness of the government systems. The PFM Reporting Framework version 2.0, includes an increased number of audit procedures to allow SAIs to audit disaster preparedness of government systems more regularly.

Expected benefits

- Identifying key PFM risk areas: The PFM Reporting Framework looks at the whole budget cycle and strives at detecting the main PFM risk areas. This ensures parliament and government can focus their reform efforts on the main identified weaknesses. It also helps the SAI to select priority issues for more in-depth audits. Identified risk areas can be the starting point for the planning of compliance, performance, or forensic audits.

- Comparing entity performance: The performance assessments are entity-specific i.e. auditors grade the level of functionality of each process in each entity. This allows comparing results between entities. When stark differences are noted, auditors can make recommendations on potential best practices based on the experiences of better performing entities.

- Understanding root causes: For each finding, auditors are encouraged to undertake a root cause analysis. This ensures that recommendations emanating from the assessments address the underlying systemic causes of underperformance.

- Understanding PFM trends: If the assessment is conducted on an annual basis, it will be possible to monitor changes and to see whether the PFM performance of the assessed entities is improving, and whether previous years’ recommendations have been implemented.

- Robust and consistent audit of SDG implementation and disaster preparedness by SAIs: The attainment of SDG targets is one of the key performance indicators of governments. The COVID19 has exposed may state institutions to be vulnerable to disaster situations in a manner that has caused great loss to life and disruptions. If the assessment is conducted on an annual basis, it will be possible to:

- monitor changes to see whether the PFM performance of the assessed entities, on the attainment of SDGs and their disaster preparedness status, is improving

- see whether previous years’ recommendations have been implemented.

- Simplicity for users: Most information needed to complete the excel table is already available through existing audit procedures. After using the tool for the first time, auditors will quickly identify what information is missing, and be encouraged to collect the missing information during their future audits.

- Clear reporting to stakeholders: On the reporting side, results on PFM are not well communicated and rarely spur debates in parliament. In many countries, the recommendations are not implemented. The PFM reporting framework is not about lengthy technical notes. It directly translates the results of the tool into a dashboard and ensures stakeholders can immediately grasp the PFM performance of each entity. The summarised information is easier to digest and more likely to encourage discussion. Progress over time can easily be monitored by external stakeholders.

Conclusion

Our gratitude goes to the SAIs who have piloted the PFM tool to date and have given us access to their PFM subject matter experts in the development of this new version. The environment in which SAIs operate are becoming increasingly complex, with high expectations on the value and benefit SAIs should have for citizens. We believe the PFM Reporting Framework tool Version 2.0, is step in the right direction towards improving the way in which SAIs are meeting their mandate to meet these expectations.

For more information and access to the PFM Reporting Framework version 2.0 and related guidance material, please contact Edmond B Shoko on [email protected]